Simple Steps to Quickly Improve Your Credit Score

Understand what makes up your credit score and discover simple steps you can take today to boost your credit score fast!

1/24/20253 min read

Why Does Your Credit Score Matter? 🤔

It matters because anytime you want to make a big purchase like a house, car, a new loan for your business, your credit score will impact the cost of borrowing money. Think of your credit score as your financial fingerprint. It's what lenders use to determine how trustworthy you are with money. A high score can open doors to lower interest rates and better terms on loans and credit cards, saving you money in the long run.

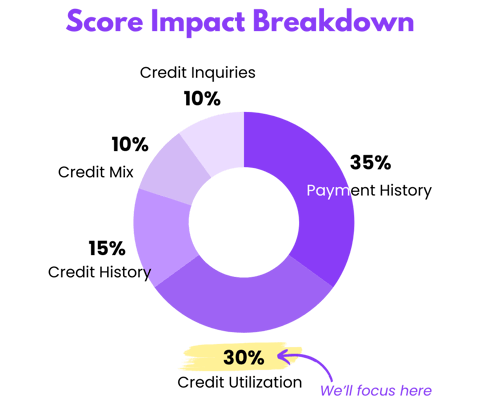

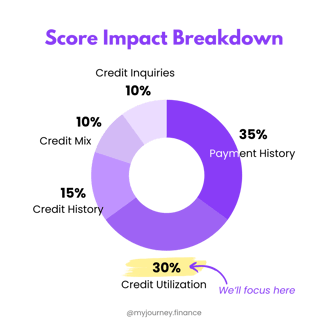

Main Factors Affecting Your Credit Score (Most to Least Impactful)

Payment History (35%) - Demonstrates if you've paid past credit accounts on time.

Amounts Owed/Credit Utilization (30%) - Indicates the total amount of credit you're using relative to your limits.

Length of Credit History (15%) - Longer credit histories are viewed more favorably.

New Credit (10%) - Includes factors like how many new accounts you have.

Credit Mix (10%) - The types of credit accounts you have (credit cards, mortgages, loans, etc.).

What can you focus on NOW to quickly boost your credit score?

Assuming you make your payments in full on time, Credit utilization✨. Since credit utiliization indicates how much of your total credit limit you're using, this can easily be adjusted to shows lenders you’re not overly reliant on credit, which leads to a better score.

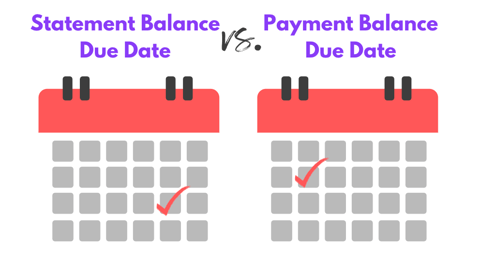

What most people do 😲: Most people wait until the payment due date to pay off their credit card bills. However you're smarter than that because now you know, what gets reported to the credit bureaus is the balance on your statement date, not payment date. To be super clear:

Statement vs. Due Date: Your statement date is when your credit card bill is issued, and your due date is when the payment is due. The balance on your statement date is reported to the credit bureaus, not what is left on the due date. Typically statement due date is around 20-25 days prior to the payment due date.

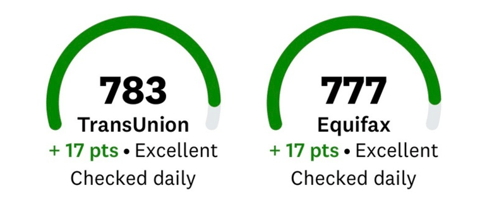

👉 So what should YOU do? I'll show you what I did to boost my score almost +17 points in one month!

Pay Before the Statement Date: To lower your utilization, make a payment before the statement date so that a lower balance is reported to the credit bureaus. For example, if your statement date is the 10th of each month and you typically owe $1,000, try to pay down most of this balance before the 10th.

Keep Overall Utilization Low: Aim to keep your overall credit utilization under 30%. If you have a $10,000 limit across all cards, try to maintain a total spent balance of no more than $3,000 at any time. I'm a bit conservative so I try to keep this below 10%. If for some reason you can't reduce your expenses, you can always call your bank and ask to increase your credit limit. 👍

Hope this helps! Feel free to reach out to me at sam@pennyandpurpose.com if this worked for you! Of course if you're feeling nice and want to drop a hello, I'd love that as well. 🫶

x PP

Look after the pennies, and the dollars will take care of themselves🙂

Penny and Purpose

"Look after the pennies, and the dollars will take care of themselves." 🙂

Join if you want more tips, strategies, and resources on business, finance, and investing! 📚 →

© 2024. All rights reserved.