Opening These 3 Accounts Transformed My Finances

Learn how opening three crucial financial accounts transformed my finances, providing significant growth and stability. 🌱

1/28/20256 min read

Every year, I take a moment to audit my finances, and I've identified three types of accounts that have significantly impacted my financial health. Below is a breakdown of why they matter and how they’ve benefitted me. I hope this makes a difference in your financial journey too. Let’s jump right in! 🙂

1. HYSA - High Yield Savings Account

Why It's a Game Changer: Leaving extra cash in a standard checking account means you’re barely earning anything, less than 1% on average. In other words, you’re lending the bank money… for free. By switching to a High Yield Savings Account (HYSA) with an average 4% return (as of early 2025), you’re not just saving, you’re earning substantially more. If you’re wondering, “what’s the catch?” it’s as simple as these institutions save on costs by not having physical branches, passing those savings to you through better rates. It’s a win win for everybody!

Let’s break it down: Imagine you put $5,000 into a High Yield Savings Account (HYSA) instead of a standard checking account. With the HYSA, at a 4% annual interest rate, that $5,000 could grow to about $16,217 in 30 years, simply by having your money sit there. In contrast, the same amount in a checking account with a 0.07% interest rate would only grow to about $5,106 over the same period. That’s a difference of about $11,000 for simply moving your money over to a HYSA. Now that’s what I call having your money work for you.

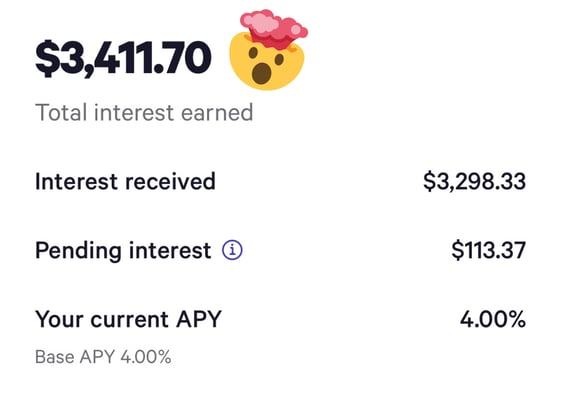

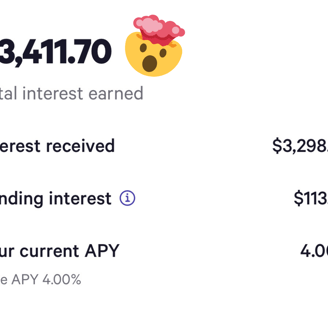

If you’re curious: On average I had about $40,000 in my HYSA and I’ve made $3,412. Interest rates also fluctuated but the average APY was 4.5%. Not bad at all in my books. I use Wealthfront and I’ve been in love with the product and user interface. It’s super easy to connect my bank account and make automatic transfers every month depending on what I want to save for e.g. emergency fund, travel fund, wedding fund, you name it. It’s such a great product and I’ve told my close friends and family about it and they love it too. For the first three months, they were able to benefit from a 0.5% boost using my referral and I’m happy to share it with you too 🙂 HERE. There are other competitive HYSA account in the market so make sure to do your research!

2. Roth IRA

Why It's a Game Changer: A Roth IRA gives you tax free growth and tax free withdrawals in retirement, which is unlike most investment accounts. How does this compare to a regular IRA or 401K? Well come retirement typically at age 59 1/2, when you withdraw money from your 401K or IRA, you get taxed on that withdrawal at your ordinary income tax rate. With a Roth IRA, you don’t pay any taxes on that withdrawal (because you already paid it when you made contributions in prior years). Roth IRA is most beneficial when you believe your income will grow over time. Why? Assuming your income will grow over time, you essentially pay less taxes now and reap the benefits later when you withdraw at a higher tax bracket. Also as a sweet cherry topper, if you’re concerned about flexiblity, you’re able to withdraw your contributions only without any penalties because the contributions you made are after tax dollars.

I want to point out, TIME is your biggest asset. Besides the common reason where you’re not able to get it back, it’s your best friend when it comes to generating returns. The earlier you’re able to save, the more time you give your money to grow. And as you know, growth isn’t linear, it is exponential.

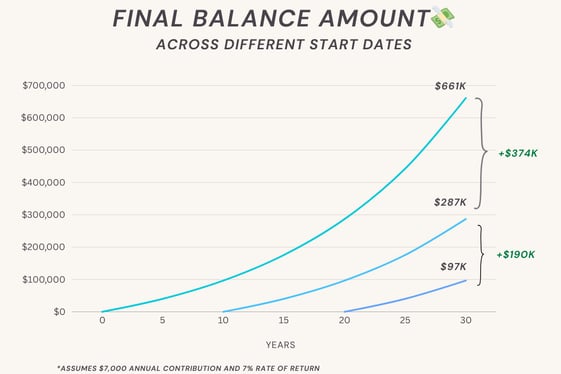

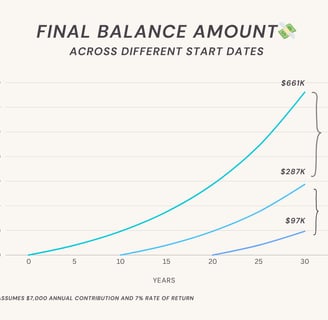

Let’s break it down: If you contribute $7,000 annually to a Roth IRA for 30 years with an average growth rate of 7%, you’ll accumulate about $661K by the end of that period. Starting the same contributions 10 years later yields $287K, and beginning 20 years later results in just $97K. The difference between starting at 10 and 20 years—$190K—shows how important early years are in compounding. To make things more interesting, extending your investment from 20 to 30 years nearly quadruples your returns from $287K to $661K, demonstrating the exponential growth potential of longer term investing. Two great lessons from this 1) early savings are slow in the beginning but sets the stage for 2) your investments, by feeding it more time, can AMPLIFY your financial position. That is the chef's kiss of exponential growth.

if you’re curious: I use Charles Schwab to house my Roth IRA, regular investing account, and checking account. There are so many reasons why I love using them but the main reason why I initially opened an account with Charles Schwab is because of their checking account. Their checking account offers amazing features like no monthly fees, no overdraft fees, and unlimited ATM fee rebates. The last point is a game changer ESPECIALLY for travel. When I need to pull money out, any ATM fees associated with pulling out cash gets credited back to you. How amazing is that?! I don’t have to stop by the airport money exchange booths and get charged extra fees anymore! If you want to open a Roth IRA or even a checking, feel free to check out Charles Schwab.

3. HSA - Health Savings Account

Why It's a Game Changer: HSA offers a triple tax advantage, which significantly enhances their value. What does triple tax advantage mean? It means:

Your contributions are tax deductible → reducing your taxable income.

The growth of your funds within the HSA is tax free → any interest or gains do not incur taxes.

Withdrawals for qualified medical expenses are also tax free → allows you to use the funds without paying any taxes on them.

You are essentially getting a tax benefit every step of the way from the moment you contribute money to using it for medical expenses. Also, many employers contribute to your HSA, which ultimately means free money that can further your savings. For 2025, the HSA contribution limit for individuals is $4,300. If your employer contributes $1,000 towards your HSA, your personal contribution requirement drops to $3,300, maximizing the benefits without maxing out your own contributions. Woot!

Let’s break it down: Suppose you are considering whether to go with an High Deductible Health Plan (HDHP) with an HSA or a low deductible plan. If you are relatively healthy and rarely visit doctors, the HDHP with an HSA might make more financial sense due to lower premiums and tax savings. You could save the difference in premium costs in your HSA, gaining interest tax free. And the best part is, the money in your account will continue to rollover every year if you don’t use it.

On the other hand, if you have regular medical needs or anticipate needing frequent medical care, a low deductible plan might be more practical despite higher premiums because it minimizes out of pocket costs throughout the year.

If you’re curious: I recently made the switch to a HDHP with an HSA since I rarely visited the doctors the past few years. There were some out of pocket expenses I had to make but I saved the receipts so I can reimburse myself later. For now, I’m deciding to front the cost now so I can let my HSA grow tax free 😉.

And that’s about it! As always, I’m here to share my personal finance experiences so you’re better equipped to make smart financial decisions yourself. If you ever want to chat, feel free to email me at sam@pennyandpurpose.com 👋!

Penny and Purpose

"Look after the pennies, and the dollars will take care of themselves." 🙂

Join if you want more tips, strategies, and resources on business, finance, and investing! 📚 →

© 2024. All rights reserved.